by cstem1121 | Mar 4, 2025 | Algorithmic Quant Intelligence, Intelligent Risk Mitigation

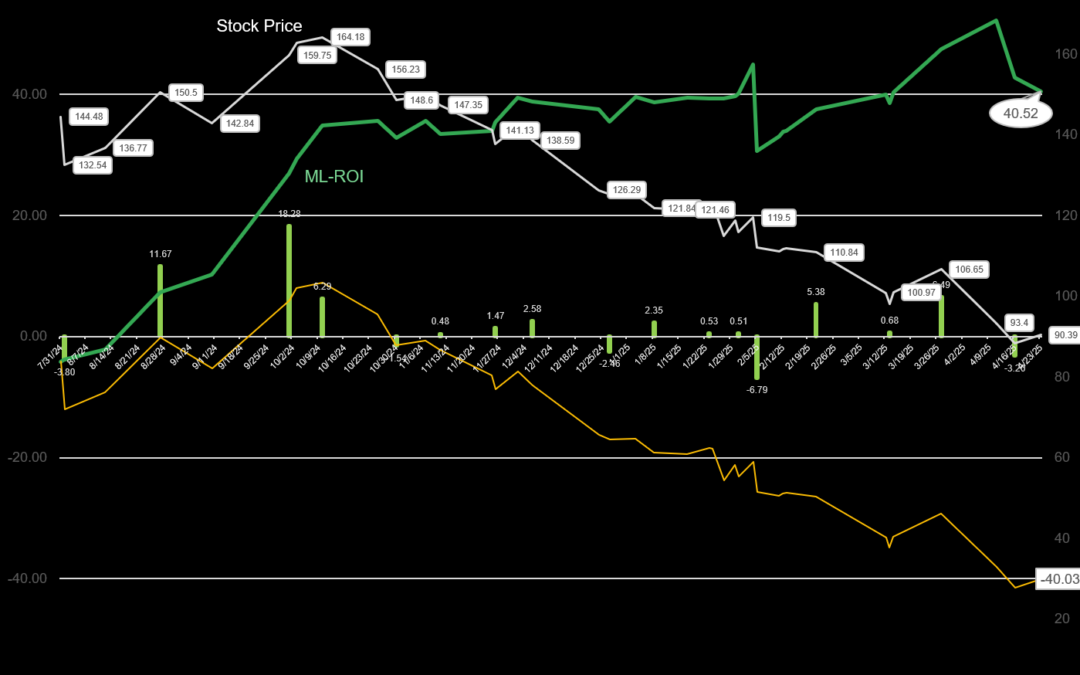

This report demonstrates the performance of Alpha Q, an adaptive machine learning (ML)-based trading system, during a bearish market cycle using AMD as a case study. The system outperformed traditional buy-and-hold strategies by leveraging high-confidence trade...

by cstem1121 | Nov 10, 2024 | Symbiotic Intelligence

The integration of artificial intelligence in stock trading has transformed how market data is analyzed and utilized. Among AI technologies, Large Language Models (LLMs)—such as OpenAI’s GPT series, Gemini, and Claude—have gained traction for their natural language...

by cstem1121 | Nov 9, 2024 | AI Investing

The integration of artificial intelligence in stock trading has revolutionized how data is processed, analyzed, and utilized for making investment decisions. Among the different types of AI technologies, Large Language Models (LLMs) like OpenAI’s GPT series have...